Stablecoin, Regulatory Clarity, and the Future of Global Digital Finance

As the global economy becomes increasingly digital and interconnected, there is growing demand for payment systems that are faster, economical, and more accessible across borders. This need is particularly pronounced in developing countries, where high remittance costs, limited access to formal financial services, and inefficiencies in cross-border transactions continue to constrain economic opportunities and inclusive growth. Against this backdrop, digital financial innovations have attracted increasing attention from policymakers, development institutions, and the private sector as potential tools to support financial inclusion, facilitate international trade, and strengthen participation in the global economy.

The role of stablecoins within the Web3 industry has evolved significantly since 2014, when BitUSD — widely recognised as the first stablecoin — was launched on the BitShares network. Initially, stablecoins were primarily used as trading instruments and as a solution to mitigate the extreme volatility commonly associated with cryptocurrencies. However, stablecoins are now increasingly being positioned as critical infrastructure for global payments, remittances, settlements, treasury management, and cross-border transfers.

As a digital payment infrastructure, stablecoins represented one of the earliest attempts to combine the speed and efficiency of blockchain technology with the price stability required for broader financial use cases. Nevertheless, large-scale adoption only began to accelerate in 2017 following the emergence of Tether (USDT) and later Circle’s USD Coin (USDC). These assets were designed to maintain a 1:1 peg with the US Dollar and were backed by cash reserves or short-term securities, offering a practical solution for businesses and individuals seeking to avoid the high volatility of cryptocurrencies such as Bitcoin.

This development enabled innovation on a much larger scale, ultimately leading governments and financial institutions to increasingly view stablecoins as part of the broader digital financial system. Stablecoins such as USDT and USDC became efficient alternatives for traders seeking to move in and out of positions without relying on traditional banking systems. At the same time, the rapid growth of DeFi protocols between 2020 and 2022 significantly expanded the role of stablecoins across the digital asset ecosystem. Stablecoins increasingly became integrated into collateral lending, liquidity provisioning, settlement infrastructure, and digital payment systems.

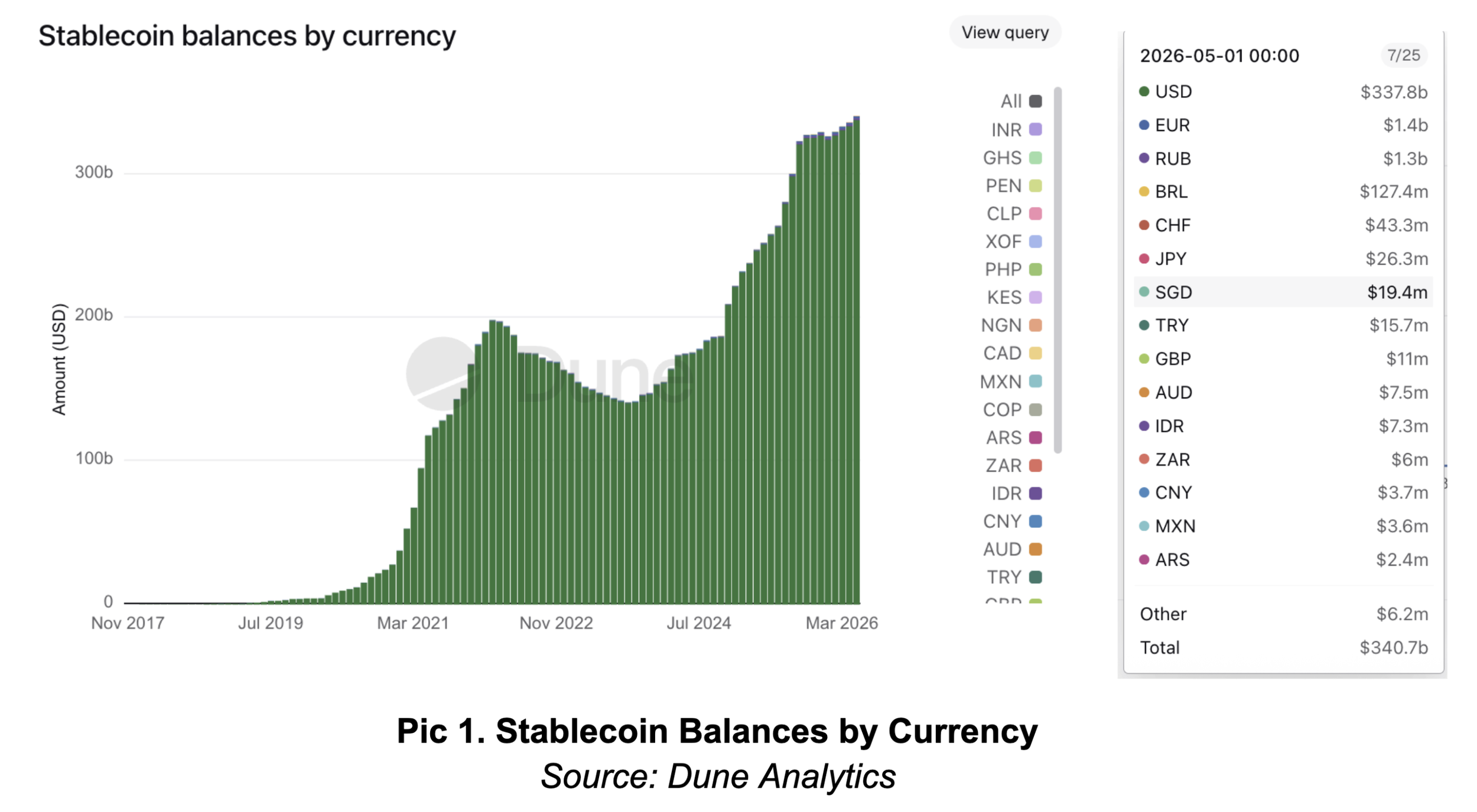

Several emerging economies — particularly in Southeast Asia (Indonesia and the Philippines), Latin America (Brazil and Argentina), and parts of Africa such as Nigeria — have also experienced notable levels of stablecoin adoption. In many of these regions, stablecoins are increasingly used as both a faster payment alternative and a hedge against inflation or local currency instability. This transformation has gradually shifted market perception. Stablecoins are no longer viewed solely as derivative products of the crypto market, but increasingly as digital monetary infrastructure with tangible utility within the global economy.

The growing adoption of stablecoins and other digital assets demonstrates both the potential and the structural challenges associated with blockchain-based financial systems. Concerns surrounding the industry intensified following several major events, including the collapse of Terra/LUNA, the temporary depegging of USDC during the Silicon Valley Bank crisis, and ongoing questions regarding the reserve transparency of several major stablecoin issuers. These incidents highlighted the extent to which stablecoin stability depends on reserve quality, liquidity management, and overall market confidence.

Recent research has also shown that different stablecoin models carry different risk characteristics. Fiat-backed stablecoins tend to exhibit greater resilience, whereas algorithmic stablecoins are generally more vulnerable to becoming systemic “risk amplifiers” during periods of market stress.

At the same time, regulators have increasingly raised concerns regarding money laundering, shadow banking activities, threats to monetary sovereignty, and the growing global dependence on privately issued digital dollars. As a result, regulators across multiple jurisdictions have begun developing frameworks designed to support innovation while simultaneously providing legal certainty, maintaining financial stability, and strengthening consumer protection.

During the early stages of the crypto industry, governments largely adopted defensive regulatory approaches. Legal uncertainty frequently placed digital assets within regulatory grey areas, particularly regarding asset classification and jurisdictional oversight. However, this approach has gradually begun to shift over the past several years.

An increasing number of jurisdictions are now developing formal regulatory frameworks aimed at integrating digital assets into the broader financial system. This transition is particularly evident through the introduction of the Markets in Crypto-Assets Regulation (MiCA) in the European Union, the Clarity ACT in the United States, and various regulatory initiatives emerging from Singapore, Hong Kong, and the United Arab Emirates.

The European Union has become one of the first major jurisdictions to establish a unified regulatory framework for digital assets through MiCA. The regulation introduces several key principles that significantly reshape how crypto-related businesses operate, including consumer protection standards, reserve requirements, transparency obligations, licensing requirements for Crypto-Asset Service Providers (CASPs), and specific stablecoin regulations designed to oversee issuers more effectively.

MiCA also categorises digital assets into several classifications, including E-Money Tokens (EMTs), Asset-Referenced Tokens (ARTs), and utility tokens. This framework is particularly significant because it provides legal certainty for crypto companies and financial institutions seeking to participate within the digital asset industry. Importantly, MiCA is increasingly viewed not merely as a restrictive regulatory framework, but as a form of institutional legitimisation for the crypto industry. Greater regulatory clarity is expected to encourage broader institutional participation, particularly across payment and stablecoin-based settlement sectors.

In contrast to the European Union, the regulatory landscape in the United States has historically remained fragmented. Jurisdictional conflicts between the Securities and Exchange Commission (SEC) and the Commodity Futures Trading Commission (CFTC) created significant uncertainty regarding whether digital assets should be classified as securities or commodities, which agency should serve as the primary regulator, and how crypto companies should operate within legal boundaries.

This uncertainty ultimately contributed to the emergence of the Digital Asset Market Clarity Act, commonly referred to as the Clarity ACT. The Clarity ACT aims to establish clearer regulatory guidance regarding digital asset classifications, jurisdictional responsibilities between the SEC and CFTC, and compliance pathways for crypto-related businesses. One of its most notable objectives is ending the era of “regulation by enforcement,” which many industry participants argue has hindered innovation within the United States digital asset sector.

Supporters of the legislation believe that improved legal certainty could strengthen investor confidence, attract institutional capital, and prevent crypto innovation from migrating outside the United States. However, critics have also raised concerns regarding potential regulatory loopholes, money laundering risks, and the ongoing challenges associated with supervising DeFi protocols and stablecoin yield products.

The evolution of crypto regulation has increasingly developed into a form of geopolitical financial competition. Several jurisdictions — including Singapore, Hong Kong, and the United Arab Emirates — are actively positioning themselves as global digital asset hubs. Singapore continues to pursue an institutional sandbox approach, Hong Kong has accelerated its Web3 hub strategy, while the UAE has adopted increasingly pro-innovation regulatory policies.

Regulatory clarity is now becoming a critical factor in attracting crypto startups, liquidity providers, institutional investors, and global payment companies. Jurisdictions capable of balancing innovation, consumer protection, and legal certainty will likely emerge as the financial centres of the next-generation digital economy.

Stablecoins are also increasingly being viewed as a new settlement layer for the global financial system. Their advantages include faster cross-border transfers, lower transaction costs, global interoperability, and the ability to support programmable finance through smart contracts. Over time, stablecoins may play an increasingly important role across cross-border settlements, remittance infrastructure, treasury settlements, tokenised finance, and the integration of Real World Assets (RWAs). This positions stablecoins as one of the most strategic components within the evolution of digital finance.

Despite their growing potential, stablecoins continue to face several critical challenges, including reserve transparency, liquidity stress, depegging risks, centralisation concerns, and dependence on traditional custodial institutions.

In addition, the emergence of Central Bank Digital Currencies (CBDCs) may create direct competition with privately issued stablecoins. As a result, the long-term future of stablecoins will likely depend on the industry’s ability to improve transparency, strengthen risk management systems, and integrate more mature regulatory standards.

Ultimately, the evolution of stablecoins reflects the broader transition of the crypto industry toward a more institutional phase of development. Regulation is no longer viewed solely as a barrier to innovation, but increasingly as a foundational component for enabling wider adoption.

MiCA in Europe and the Clarity ACT in the United States demonstrate how governments are beginning to integrate digital assets into the global financial system in a more formal and structured manner. Over the long term, regulatory clarity will likely become one of the defining factors determining which jurisdictions emerge as global centres of digital asset innovation, how stablecoins are integrated into the global financial system, and how blockchain technology evolves as foundational infrastructure for the next generation of the digital economy.

Lydia Tri Puspita, Blockchain Analyst